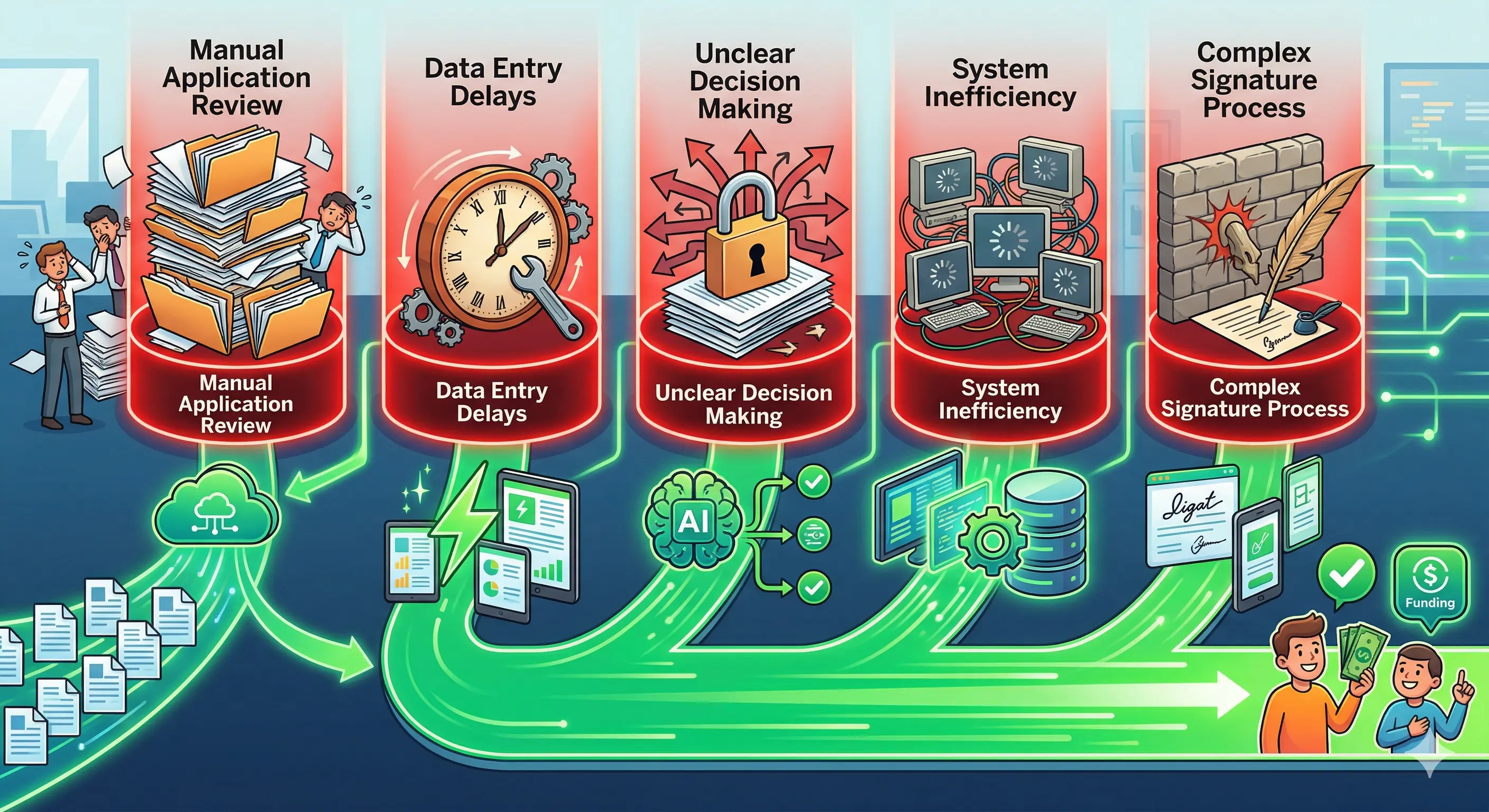

5 Loan Origination Bottlenecks and How to Eliminate Them

Slow loan origination costs deals and frustrates borrowers. Identify the five most common bottlenecks in commercial lending and learn proven strategies to fix them.

Speed Wins Deals

In commercial lending, origination speed is a competitive advantage. Borrowers with time-sensitive acquisitions, construction timelines, or refinancing windows don't wait around for slow lenders. Yet many lending teams operate with workflows that haven't fundamentally changed in a decade.

Here are the five most common bottlenecks—and what to do about them.

1. Document Collection and Triage

The problem: Borrower packages arrive piecemeal over days or weeks. Documents are emailed as attachments, uploaded to portals, or even faxed. Once received, someone has to open each file, determine what it is, and check it against requirements.

The fix: Implement a centralized upload portal with automated document classification. When borrowers upload files, AI identifies each document type and maps it against the deal checklist. Missing items surface immediately, enabling targeted follow-up on day one instead of week two.

The impact: Document intake that took 30–60 minutes per deal drops to under 5 minutes. Missing document identification happens at upload, not when an analyst finally opens the file.

2. Financial Spreading

The problem: Manual spreading is the single most time-consuming analyst task in commercial lending. Keying numbers from PDFs into spreadsheets takes 2–4 hours per deal and introduces transcription errors that compromise ratio analysis.

The fix: AI-powered spreading extracts data directly from financial documents, maps line items to your standardized template, and flags anomalies. Analysts review the output instead of creating it from scratch.

The impact: Spreading time drops from hours to minutes. Error rates decrease because the primary source of errors—manual data entry—is eliminated.

3. Policy and Screening Checks

The problem: Most institutions have lending policies that define acceptable ranges for key metrics—debt service coverage, leverage, industry concentrations, minimum credit scores. Checking a deal against these policies is often a manual process of comparing numbers to a policy document.

The fix: Automated policy screening compares borrower metrics against your institution's lending criteria as soon as spreading is complete. Exceptions are flagged immediately, and the screening results feed directly into the credit memo.

The impact: Policy compliance is checked in seconds rather than hours. Deals that don't meet criteria are identified early, before significant analyst time is invested. Exception documentation is generated automatically.

4. Credit Memo Preparation

The problem: Credit memos are comprehensive documents that synthesize data from multiple sources—financial spreads, ratio analysis, screening results, industry research, and collateral information. Writing one from scratch takes 4–6 hours and is the primary reason deals sit idle before committee.

The fix: AI-assisted memo generation pulls data from completed spreads and screening results to draft structured memos in your institution's format. Analysts review and refine rather than writing from scratch.

The impact: Memo preparation time drops by 70–80%. Memos are more consistent across analysts, and committee cycles shorten because memos are ready sooner.

5. Pipeline Visibility

The problem: Without a unified view of the deal pipeline, managers can't identify where deals are stuck. Individual analysts may have deals sitting in their queue that they haven't started, or deals may be waiting on a single missing document that no one has followed up on.

The fix: Implement a deal pipeline that tracks every deal from intake through approval. Each stage should show what's complete, what's pending, and how long the deal has been in its current stage. Automated alerts flag deals that have been idle too long.

The impact: Management gains real-time visibility into pipeline health. Bottlenecks are identified and resolved before they become problems. Deals don't fall through the cracks.

The Compounding Effect

These bottlenecks don't exist in isolation. A delay in document collection pushes back spreading, which delays screening, which delays the memo, which delays committee. Fixing any single bottleneck improves the whole pipeline—but fixing all five transforms it.

The lending teams that close deals fastest aren't necessarily the ones with the most analysts. They're the ones that have eliminated the dead time between each step in the origination process.